(Image Source: Jason Pofahl / Unsplash)

Wisconsin IDEA

Insight • Data • Economics • Analysis

From Concerns of Recession to Potential ‘Soft Landing’

When the Federal Reserve Bank began raising interest rates to combat inflation in March 2022, coupled with lingering effects of the COVID-19 pandemic, such as continued issues with supply chains, fears of an economic recession began to rise. Numerous leading economic indicators, such as the yield curve, which compares short- to long-term interest rates and the University of Michigan’s Consumer Sentiment Index, pointed to a pending recession. The Conference Board’s composite index of leading economic indicators turned consistently negative and has been declining for several months proving a strong single of a forthcoming recession.

Then in March of 2023, three medium-sized banks failed: Silicon Valley in California, Signature Bank in New York and Silvergate Bank also in California. While these banks failed for a variety of reasons, such as over-exposure to older US debt instruments paying lower interest rates in a period of rising rates (Signature) to cryptocurrencies (Silvergate) to general mismanagement of risk to slow responses of government regulators, there was concern that the underpinnings of the US financial institutions were weak. Memories of the collapse of the secondary financial markets sparking the Great Recession were revisited.

To gain some insights into the underlying condition of national financial markets, this issue of the Wisconsin IDEA Data Snapshot explores trends in two market condition measures: the Federal Reserve Bank of Chicago’s National Financial Condition Index and the Federal Reserve Bank of St. Louis’s Financial Stress Index. The two indices are similar in that a positive value of each index indicates tighter financial conditions (Chicago measure) or higher levels of financial stress (St. Louis measure). They differ in that the specific indicators that make up the respective indices differ. Each index is updated weekly.

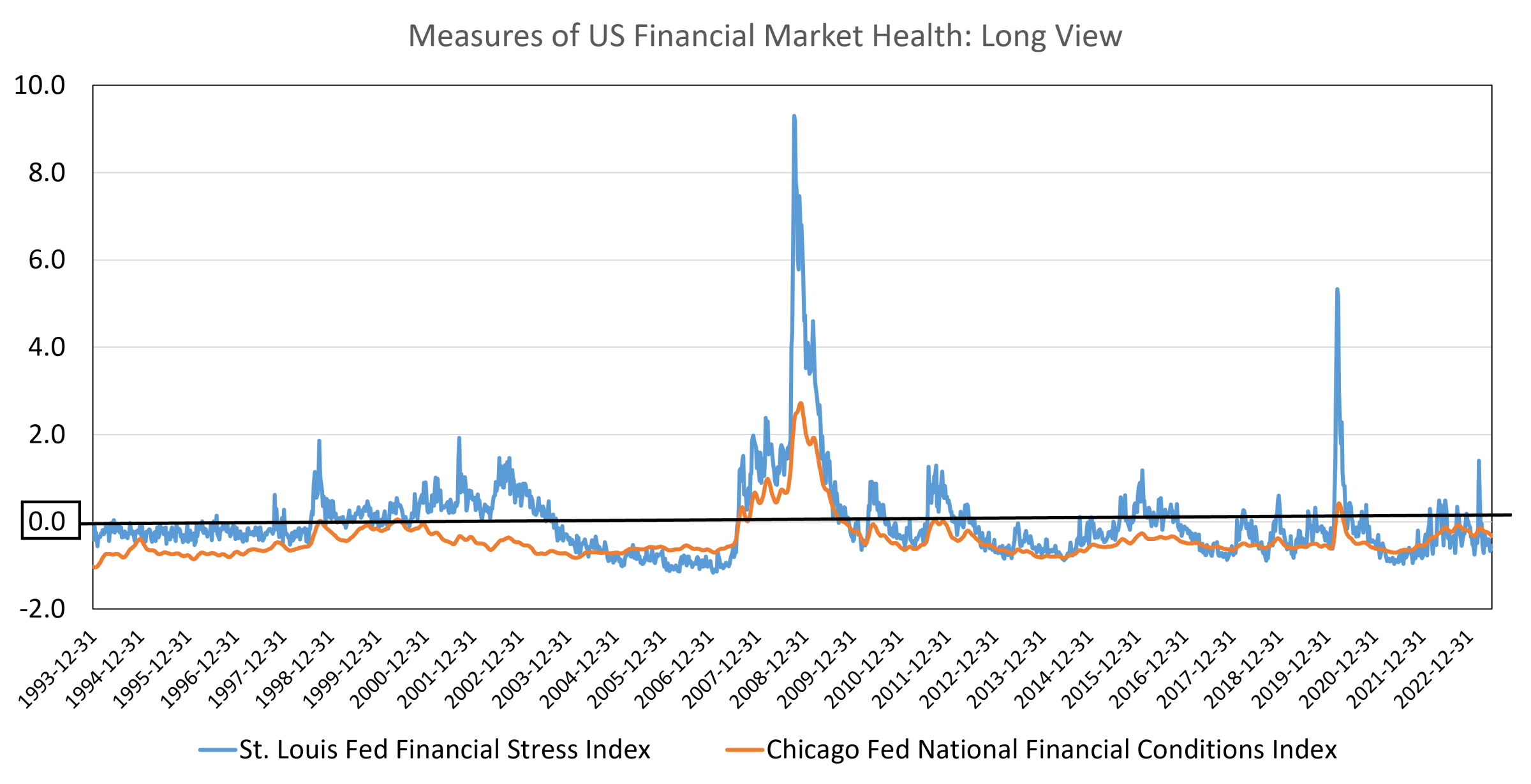

Figure 1 – Measures of US Financial Market Health: Long View

Taking the long view, it becomes clear that the St. Louis index is more volatile than the Chicago index and previous recessions are evident. Using the Chicago index, the depth and length of the Great Recession are evident and reinforce the idea that the economy was on the edge of slipping from a recession to an economic depression. In addition, there were mild setbacks to the recovery in June 2010 and September-December 2011. There is also evidence that COVID caused the recession although that shock was remarkably short.

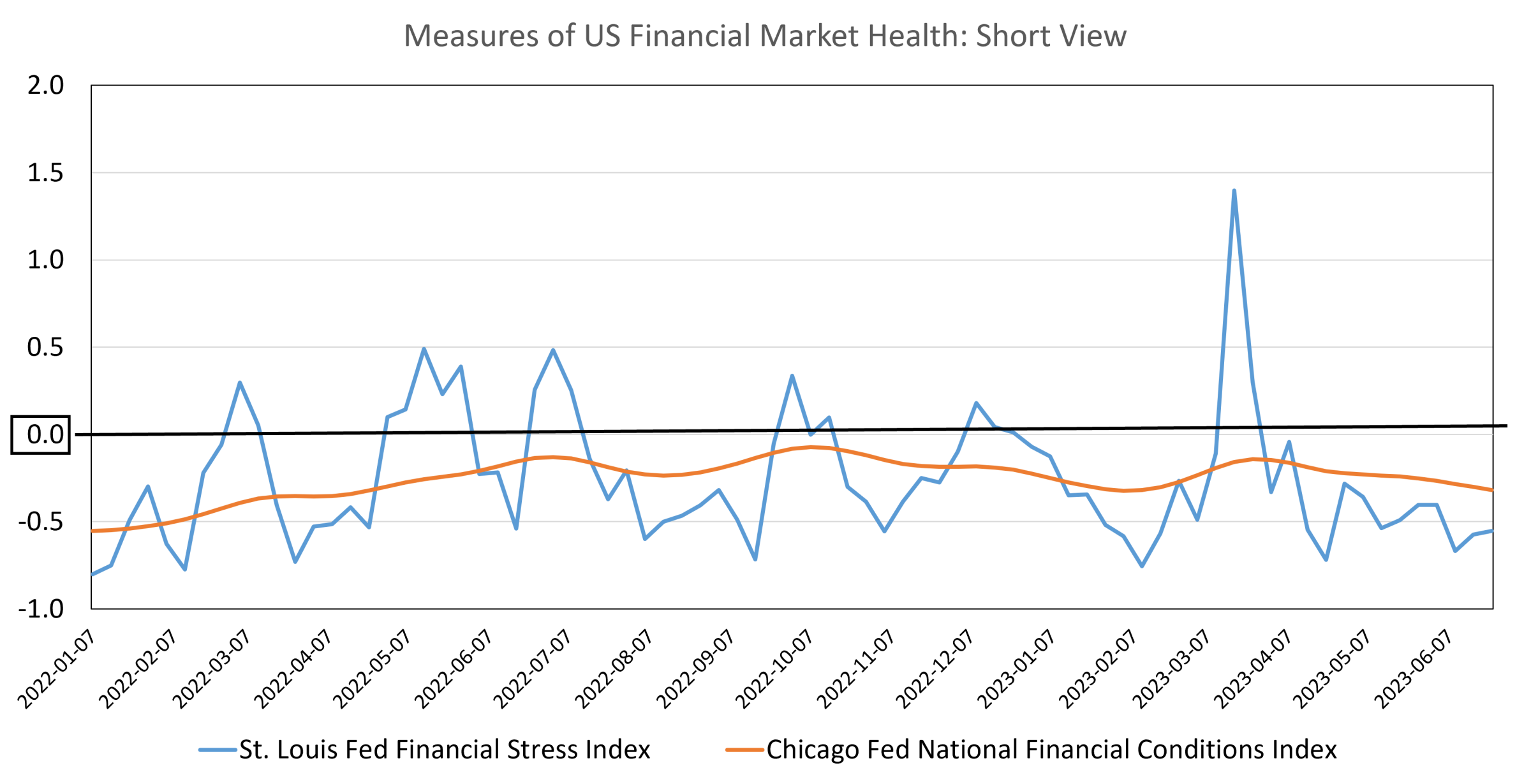

Figure 2 – Measures of US Financial Market Health: Short View

Taking a short view, the numerous, albeit brief, episodes of fiscal stress or difficulties using the St. Louis index and the three bank closures resulted in a spike in March 2023. These brief periods of difficulty identified by the St. Louis measure have contributed to the perception of an impending recession. The Chicago measure, while trending upward throughout much of 2022 and also lending support to the idea of an impending recession, remained negative, indicating that the financial markets are healthy. Perhaps more important, since the three bank failures in March 2023, the Chicago and St. Louis measures are trending downward, indicating a strengthening of the financial markets.

The recent trends in the Chicago and St. Louis measures, coupled with remarkably strong labor and housing markets, suggest that the likelihood of a recession is weakening. Given that these are only a couple of indicators and others, such as the inverted yield curve (i.e., short-term interest rates are higher than long-term rates), are signaling a recession it appears that a “soft landing” is more likely than a recession.