(Image Source: Kenny Eliason / Unsplash)

Wisconsin IDEA

Insight • Data • Economics • Analysis

How Savings Rates Drive Investment, Stability, and Future Prosperity

From a macroeconomic perspective, the net savings rate is a critical indicator of the economic health and future growth potential of a country. First, savings provide the necessary funds for investment in capital goods, such as machinery, infrastructure, and technology. Higher investment levels typically lead to higher productivity and economic growth. Further, a healthy savings rate supports sustainable economic growth by ensuring that sufficient resources are available for future investment. Second, higher savings rates can provide a buffer against economic shocks. Countries with higher savings can better withstand economic downturns, financial crises, and unexpected expenditures without resorting to excessive borrowing.

Third, adequate savings ensure that future generations have the resources needed for investment and consumption. Low savings rates can lead to underinvestment in essential areas such as education, infrastructure, and healthcare, adversely affecting future economic prospects. Fourth, higher savings allow households to smooth consumption over time, providing financial security and reducing vulnerability to income shocks. A higher net savings rate enhances the overall resilience of the economy by providing households with a cushion during periods of economic downturns and uncertainties. Other factors affected by the net savings rate include inflation and the effectiveness of monetary policy, and international trade through effects on exchange rates, among other factors.

Net Savings Trends in the U.S.

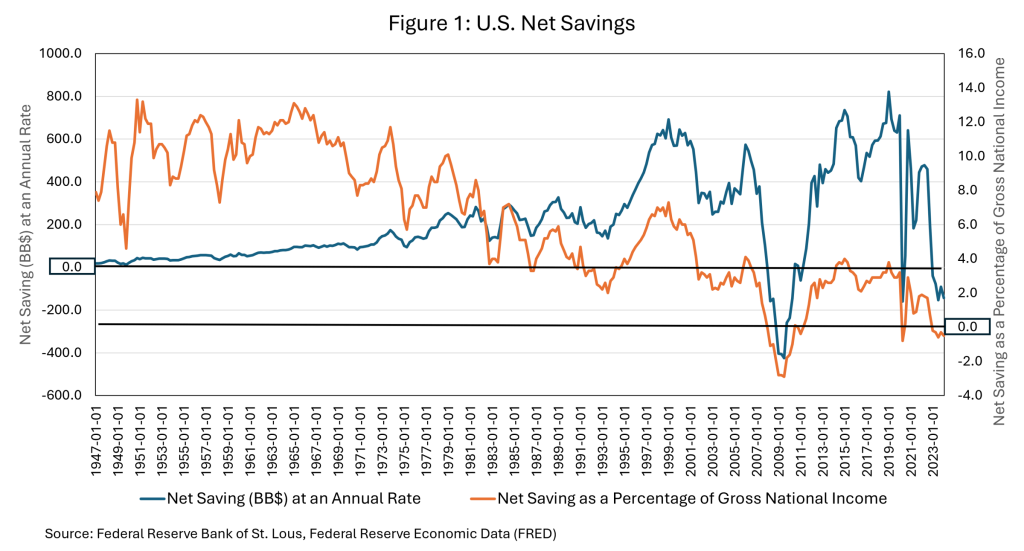

Figure 1. U.S. Net Savings

Total U.S. net savings as a percent of Gross Domestic Income (GDI) [1] has averaged 6.3 percent over the period from 1947 to the first quarter of 2024. There are, however, notable differences over that period. Throughout the 1950s and into the 1960s, the average annual net savings as a share of GDI was 10.7 percent. From 1970 to 1990, the average was 7.0 percent, but from 1990 to 2024 (first quarter), the share dropped to 2.7 percent. More recently, from 2002 to 2024, the average share was 1.8 percent, and nearly one in five quarters saw negative net savings as a percent of GDI. The most noticeable “negative savings” was spurred by the Great Recession and the last five quarters (2023 and the start of 2024).

At the same time, the overall level of net savings (annualized) has been increasing. Since 1990, the average annual net savings has been $337.3 billion, with noticeable dips during the Great Recession and the immediate start of the COVID-19 recession. These periods make sense as economic agents (households and businesses) drew down savings to make up for lost income. More concerning is the drawdown in savings over the past five quarters, suggesting that total net savings have not kept pace with overall growth in GDI and is moving in the wrong direction.

Disaggregated Data Insights

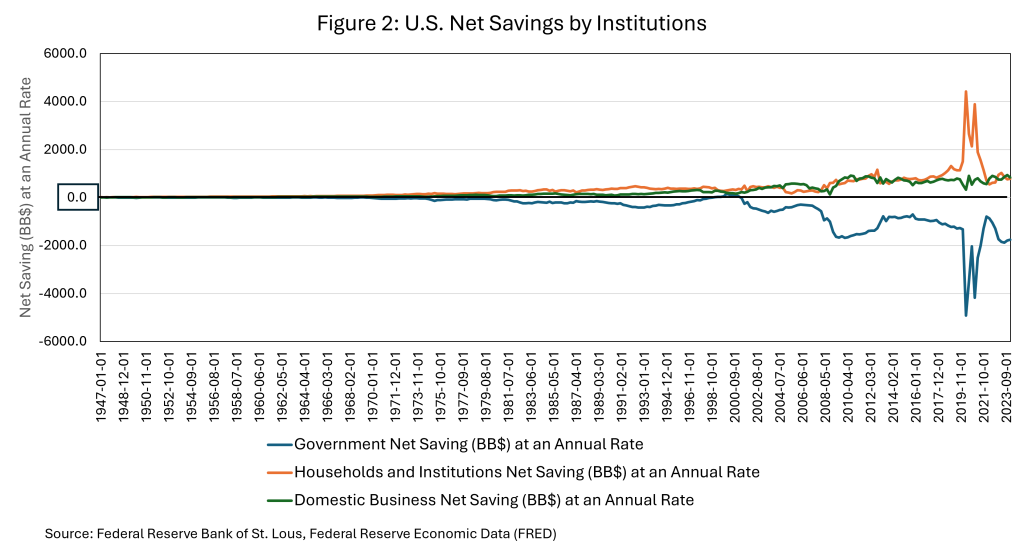

Figure 1. US Net Savings by Institutions

To gain insights into the sources of the decline in net savings, the data can be disaggregated into the savings rate for domestic businesses, households and institutions, and government. The latter tends to be dominated by the federal government but also includes state and local governments. Two patterns emerge from the data:

- The level of net savings by domestic businesses and households and institutions has been relatively stable throughout the entire period, with some evidence of a modest upward increase since the Great Recession. There was a noticeable spike in increased net savings by households and institutions during the COVID-19 pandemic, as people delayed spending and received federal stimulus payments.

- The downward trend in net savings as a share of GDI observed is largely driven by deficit spending by the U.S. federal government. From the 1970s through the 1990s, the level of federal deficit spending was relatively stable until about 2001, when it increased under the George W. Bush Administration. The Great Recession and COVID-19 pandemic both triggered significant increases in deficit spending, which has persisted in recent periods.

Long-Term Impact

The long-term impact of current rates of negative net savings is unclear. The sustainability of consistently large federal deficits is a significant concern. The potential for long-term investments, such as those from the Inflation Reduction Act (Build Back Better) and the CHIPS and Science Act, impact the economy sufficiently to offset the short-term impacts of negative net savings remains to be seen. Economists suggest that conclusions may vary depending on whether one takes a short-term or long-term view.