March 2018 — In Wisconsin, the labor market has been the focus of recent public and political discourse, with many perceiving a labor shortage. Often these discussions focus on the experience voiced by employers throughout the state. While the frustration of employers trying to hire workers is an important sign that there could be a labor issue, there are several economic indicators that can be used to assess the presence and severity of a labor shortage. These include different measures of the unemployment rate, the ratio of unemployed workers to job openings, average weekly hours worked, the labor participation rate and wage growth.

1) The Unemployment Rate

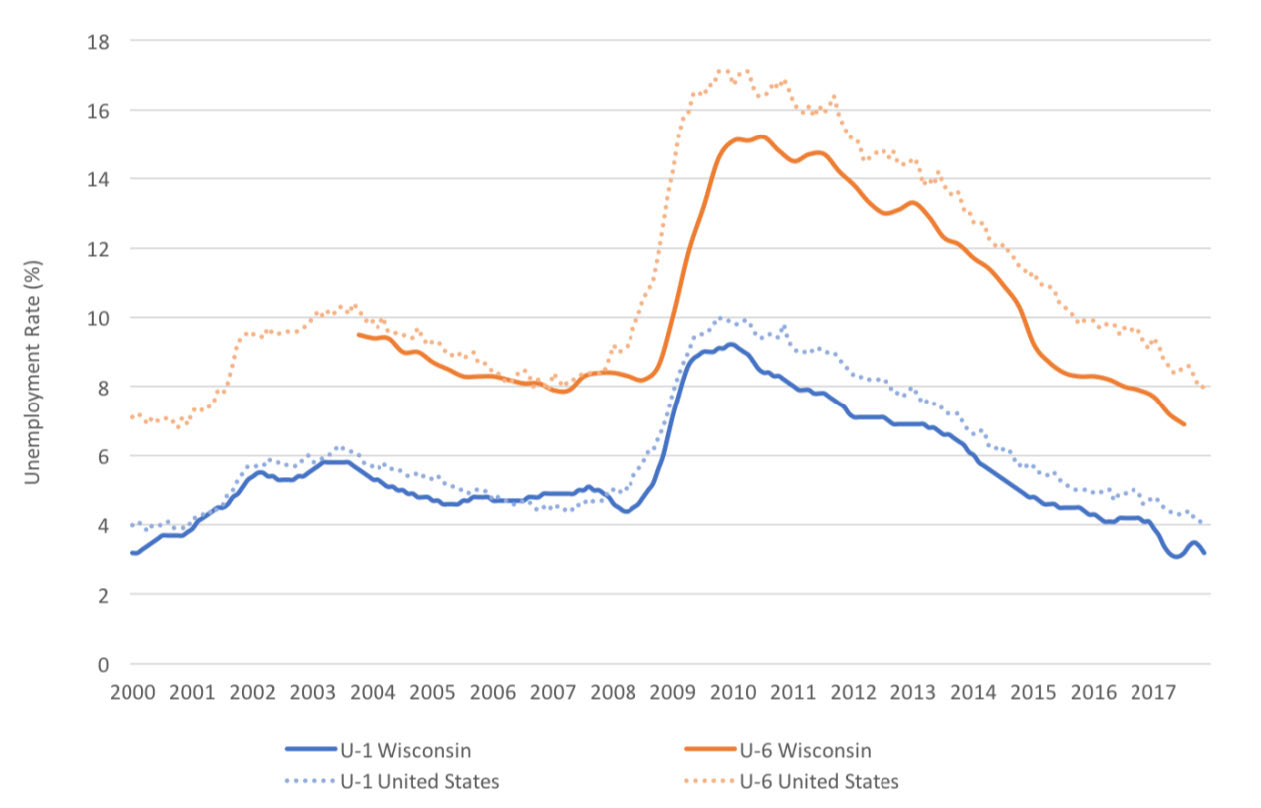

The unemployment rate measures the rate of joblessness. The most commonly reported unemployment rate is the U-1¹, which captures those in the labor force who are actively seeking employment but do not have a job. Alternatively, the U-6 rate includes not only job seekers, but also “discouraged workers” who would like a job, but have become dismayed by their prospects and quit looking for employment. Furthermore, the U-6 rate includes the underemployed, or those who have a job, but would prefer to work more hours. Given the more inclusive definition of the U-6 rate, it is typically higher than the U-1.

Wisconsin’s U-1 and U-6 rates are below the national average and quite low by historical standards, at 3.2% and 6.9% respectively. These historically low values suggest only minimal joblessness in the state. Even at “full employment,” which economists estimate is close to 4%, there is still some unemployment as people change jobs, move, and enter the work force. Wisconsin appears near full employment, but not dramatically below that point. While the large pools of unemployed residents available during the recession have eroded and there is relatively little unused capacity, declining unemployment rates are not atypical of a period of economic growth.

Figure 1: Unemployment Rates, Conventional (U-1) and Alternative (U-6) Measures, Wisconsin and U.S.

2) The Ratio of Unemployed Workers to Job Openings

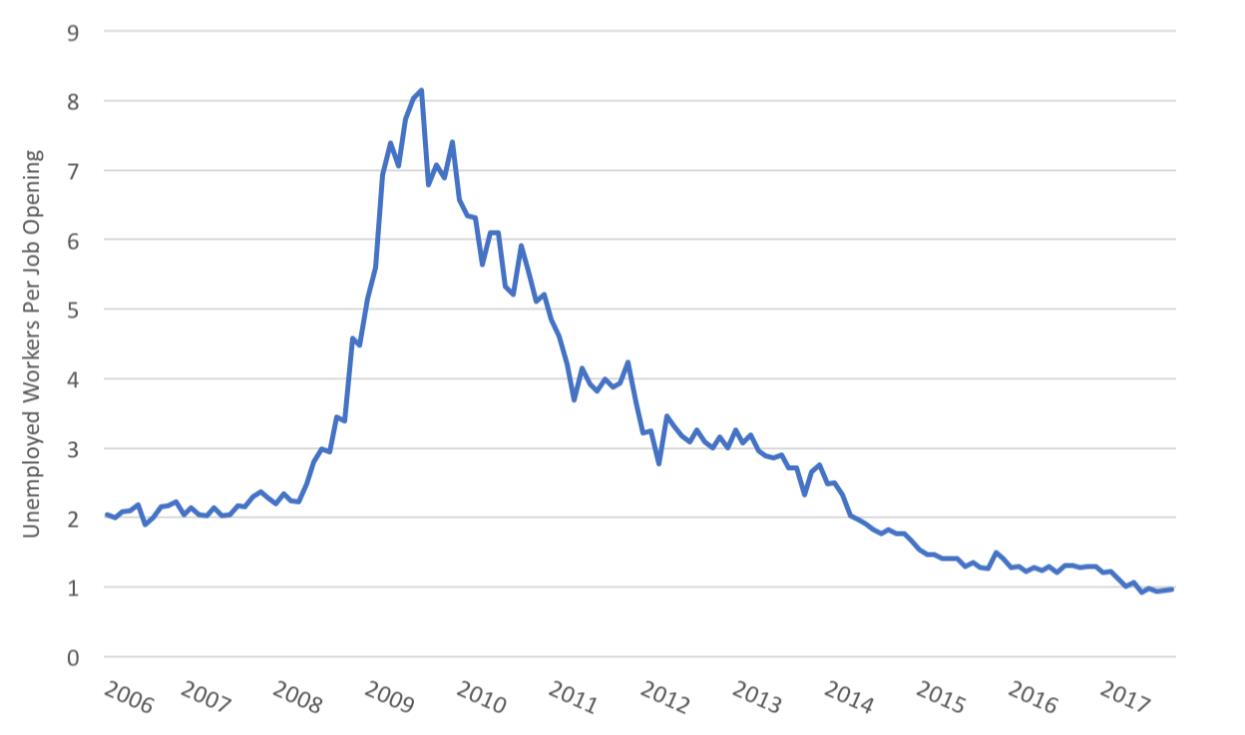

The ratio of unemployed workers to job openings measures how many job seekers there are for every unfilled position. In the Midwest, there were over eight unemployed workers per job opening at the height of the recession. During this period, employers had large pools of workers available to fill their job openings. That pool of workers has steadily become smaller as the economy has recovered and expanded, generating new employment opportunities. Most recently, there was roughly one unemployed person per job opening in the Midwest. This suggests a tight labor market where there is relatively little unused labor capacity.

Figure 2: Unemployed Workers per Job Opening, Midwest Region

3) Average Weekly Hours Worked

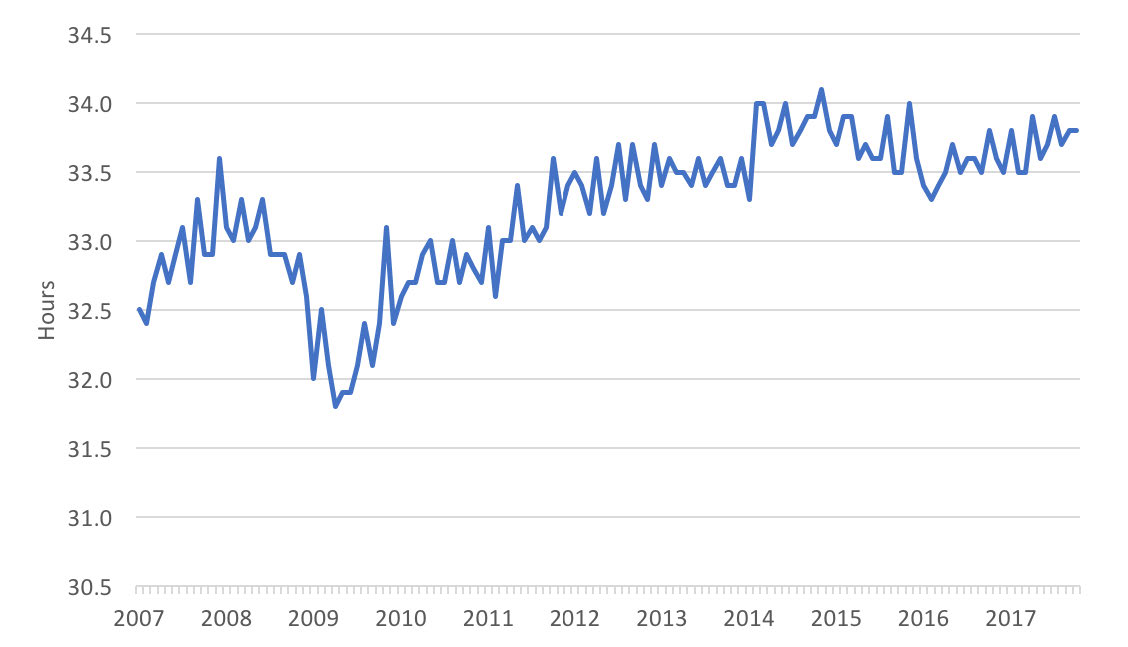

When employers cannot fill positions, they may ask or even require the workers they do have to work more hours. To the extent that there is a labor shortage, we would expect to see increases in the number of average weekly hours worked. Average weekly hours worked for private employees in Wisconsin have increased since the Recession as expected. Workers now average 33.8 hours per week which is more than the prerecession peak of 33.6 hours. However, average weekly hours worked, while exceeding prerecession levels, have been relatively stable in recent years. At 34.1 hours per week, the post-recession peak came in late 2014 and has declined slightly since then. This trend does suggest that employers are asking more of their workers than a decade ago, but the increase in hours worked has not continued. In fact, it has declined slightly. Thus, based on hours worked, there is not strong evidence of a severe labor shortage.

Figure 3: Average Weekly Hours Worked, Total Private Employment, Seasonally Adjusted, Wisconsin

4) Wage Growth

Economic theory demonstrates that prices respond to both the demand and the availability (supply) of a good or service. When a good or service is in short supply, prices tend to increase. Small, widespread growth in prices is a characteristic of a stable and growing economy. Quickly rising prices, however, can be a sign of a shortage.

Labor markets work similarly to markets for other goods and services. If workers, who are selling their labor, are in short supply, they should be able to command a higher wage. These higher wages increase the incentive to work and pull more workers into the labor force and alleviate the shortage. If employers are forced to raise wages to attract and retain workers, and this increase in wages is not offset by people entering the labor force, then there is evidence of a labor shortage.

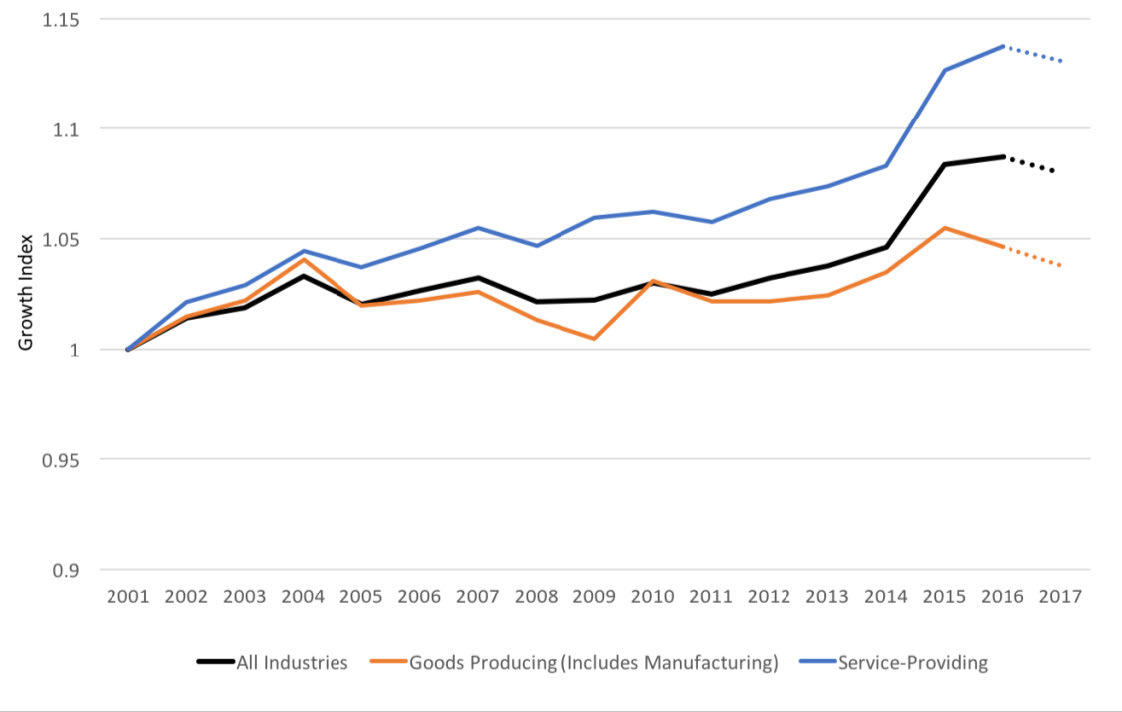

Figure 4: Real Wage Growth Index, 2017 Dollars, Wisconsin

A Note on Wage Data

Figure 4 is based on data from the Quarterly Census of Employment and Wages (QCEW). It is typically considered the most conventional, comprehensive, and reliable source of wage data, but it is not the most current. Alternatively, the Current Employment Statistics (CES) uses a much smaller sample of employers to release monthly wage estimates that are more current. Based on CES data for October and November 2017, year-over-year wage growth has increased to between 2.5-3% from near .6% in the same months a year prior.

Given this interplay between the demand for and supply of workers, the wage-based evidence of a labor shortage has been somewhat weak. While employers are offering higher wages than before the recession, both nationally and in Wisconsin, the increases have been modest. Further, some gradual wage growth over time is expected. Only in service-producing industries have wages grown considerably faster than other sectors. So while there is notable wage growth in services, which could be evidence of a shortage for workers in this sector, on the whole wage growth has been moderate at most.

It is important to keep in mind, however, that wages are just one component of employee compensation. It could be that employers are competing for workers using other methods of compensation such as offering more schedule flexibility or additional vacation days. There are also stories of employers and workers agreeing to forgo wage increases in lieu of maintaining health benefits. Indeed, employer contributions to insurance and retirement programs have been growing. These types of increases in alternative forms of employee compensation could also be symptomatic of a labor shortage, but are not captured in wage growth.

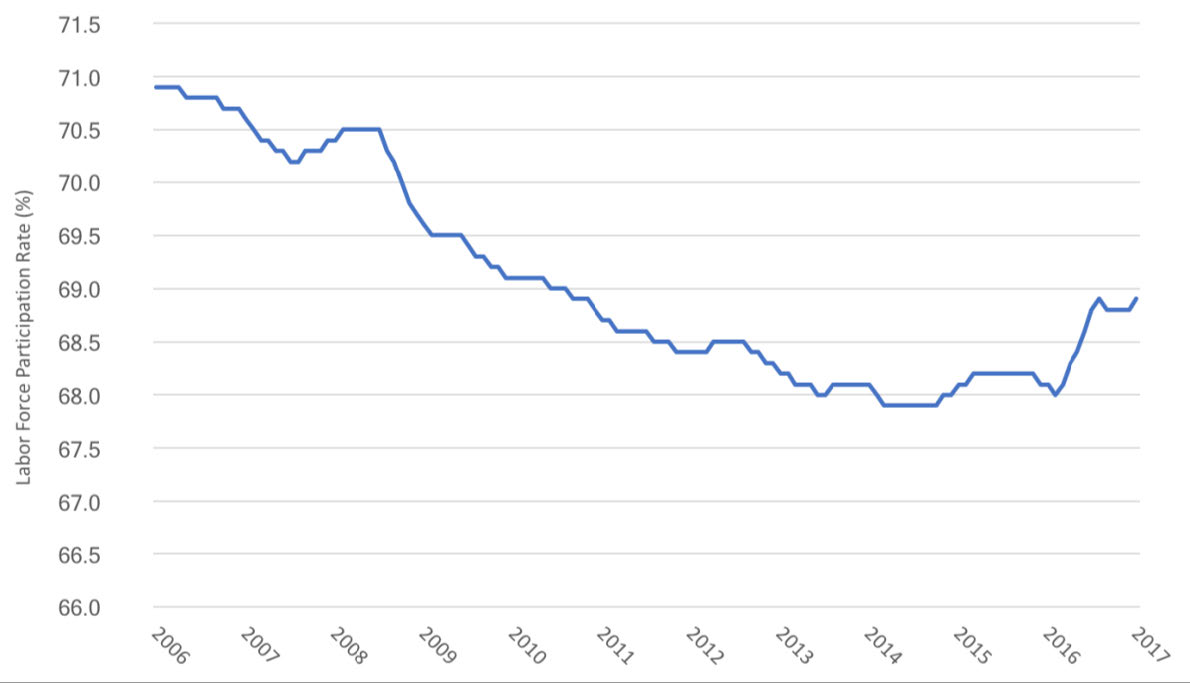

5) Labor Participation Rates

Another possible reason that we have not seen more dramatic evidence of a labor shortage is slowly growing labor force participation rates. During the recession, many workers left the labor force, exacerbating the long-term decline in the labor force participation rate partially due to Wisconsin’s aging population. In addition to typical retirement rates among older workers, some employees opted for early retirement and many others of prime working age left the labor force after long periods of unemployment, discouraged by their job prospects during the Great Recession. Furthermore, many younger workers may have elected to remain in school because of the lack of current employment opportunities and/or their decision to improve future employment prospects. Some of these people who left the labor force may have preferred to keep working and, now that job opportunities are expanding, they may be re-entering the labor force. As the number of workers seeking employment increases, these individuals may be relieving some of the pressure on the labor market and keeping wages and hours worked from growing more rapidly.

Figure 5: Labor Force Participation Rate, Wisconsin

Conclusion

Based on the unemployment rate, the ratio of job openings to unemployed workers, average weekly hours worked, wage growth and labor participation rates, it is clear that the large pool of idle labor that grew during the recession has diminished. With low unemployment and few workers to fill open positions, there is little slack in the labor supply that could be absorbed to meet a growing demand for workers. The signs of a severe labor shortage, however, are modest. When employers face a shortage, we expect them to raise wages and to ask the workers they do have to work more hours. While wages and hours worked have both increased, these increases have not yet been extreme. Employers may be benefitting from growing labor force participation, as residents, many of whom may have left the workforce during the recession, (re)-enter the labor force. Thus, while the labor market is tight, the evidence of a sizeable labor shortage currently is mixed.

That said, with little unused labor, a growing need for workers could add pressure to the labor market as the economy expands. Furthermore, the state has a large share of workers headed for retirement that could exacerbate the need for workers. This need is unlikely to be filled by new workers coming into the state given the relatively low rates of in-migration and lagging birth rates over the last decade. Given how these factors could combine with increasing labor demand, the current circumstances could evolve into a more serious labor shortage.

Also note, the analysis presented here takes a broad view of the question of a Wisconsin labor force shortage. While there is evidence of a tightening labor market, there does not appear to be an immediate crisis. This is not to say that in certain regions within Wisconsin or specific industries are not facing a more serious shortage. It may be the case that there is a surplus of workers in one geographic area of the state and a severe shortage in another part of Wisconsin. It may also be the case that some industries simply cannot offer sufficient wages to attract workers. For some industries the margins are sufficiently thin that rising wages would make them unprofitable.

End Notes

¹Only people who are jobless, looking for a job, and available for work are counted as unemployed. The labor force consists of all employed and unemployed persons. The unemployment rate, U-1, is ratio of those unemployed to the labor force. Alternatively, U-6 more generously defines the unemployed by including those who may not have recently looked for work, perhaps because of a discouraging economy, but would still like a job. For a thorough description please visit https://www.bls.gov/cps/cps_htgm.htm