April 2022 — Downtown office space is connected to the success of service businesses, housing, entertainment, and plays an important role in promoting a healthy community where people can live, work, and play. Office space is a significant component of a healthy downtown because it generates employment and daytime activity, which supports other downtown businesses such as restaurants, retail, entertainment, and personal and professional service businesses. Downtown office space also supports housing and lodging development, which in turn can help bring vibrancy to the downtown outside of normal working hours.

This section provides information and tools to assess the office market based on supply and demand. It is intended to only be a starting point, providing a preliminary market overview.

Learn more:

Related Content

Office Space Trends

Demand for office space has changed over the years. With the growth of the suburbs, many employers moved from downtown locations to the periphery to take advantage of lower rents, less expensive parking, and proximity to worker’s homes. More recently, the Great Recession forced many companies to downsize leading to high vacancy rates. Despite these forces, office space continues to be an important component in many downtowns.

Law firms, accountants, and financial advisers locate in downtowns not only because it’s important to their image, but because they need to be close to the court system and other public institutions from which they draw a portion of their business. Other types of businesses, including corporate headquarters, are attracted to vibrant downtowns for reasons associated with talent attraction. These businesses believe that locating downtown will help them compete more effectively for young, skilled professionals that are looking for more walkable, amenity rich locations in which to work and possibly live.

While some communities do find demand for downtown office space, the supply of appropriate space is often limited. Of particular concern is the mismatch between the size (square footage) of existing office buildings and the space demands of small to midsize companies and independent entrepreneurs. Downtowns may have few, if any, code compliant, affordable, and appropriately sized office spaces for the types of users that are attracted to downtown locations.

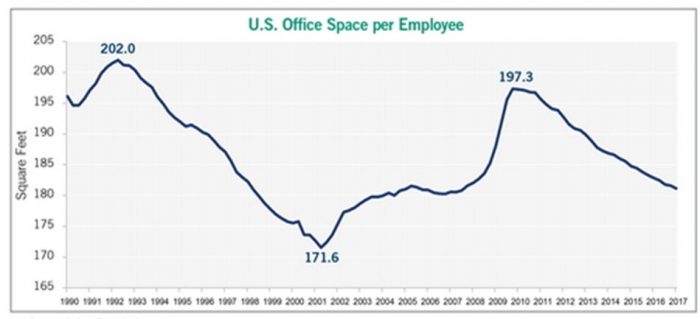

Other trends shaping the market for office space include an increase in telecommuting—that is, working from home through the use of technology—and changes in work preferences among young professionals. Smartphones and communications software diminish the need for dedicated physical offices, with many offices remaining unused for full or partial days due to remote working from a variety of locations. These trends are reasons why square footage per worker is decreasing in the United States. The following chart depicts changes in office space density per worker over time.

How we work is also impacting office design. Traditional cubicle and doored offices have been replaced by open plan offices designed to promote communication and collaboration and are characterized by shared desk space and technology functions. Amenities such as fitness centers, shared kitchens, pet facilities and lounge areas are also being incorporated into new and repurposed office space reflecting changes in consumer demand.

Office Space Supply

Inventory

The current supply of office space provides a basis for assessing market conditions in a community. In order to assess the supply of office space, it is important to take an inventory of existing office stock. Depending on the community, it may be important to analyze not only the downtown area but also the surrounding trade area if there is competitive office space located there. In smaller communities, much of the quality building stock might be located at the edge of town and it is important to note how that affects the downtown office environment.

Important factors to include in an inventory are location, unit quantity, size, and class of office space in the community.

- Location: Smaller communities’ office locations can be identified by address or identified on a map. For larger communities or regions, GIS can be used to plot office employment using data from sources such as the Census Bureau’s On the Map. This exercise is useful in terms of understanding the spatial distribution of office space but is not critical to the market analysis.

- Unit Quantity: The number of office buildings in the downtown and market area should be estimated if possible. This may not be feasible for large communities, but it is for smaller communities.

- Size: The total square footage of office space should be estimated and tenants recorded. For larger communities, this data is available through quarterly reports produced by organizations such as Newmark Knight Frank. For smaller metro and rural areas, the analyst must compile the data painstakingly. Methods to do so include talking with local realtors, business owners, and property owners. Google Earth can also locate office buildings within the community and estimate square footage using the polygon tool.

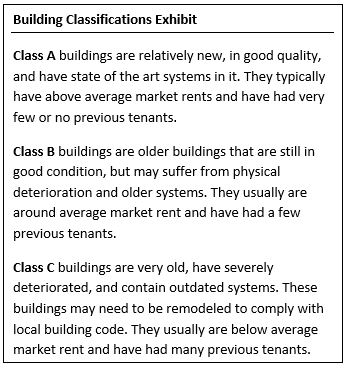

- Class: Properties are assigned a class that categorizes the current conditions and overall quality of office space. Office buildings are divided into three classes: A, B, and C. Depending on the size of the community it may not be realistic to assign a class to each office property; however, the downtown analyst should have a general understanding of where different classes of office buildings are found throughout the trade area.

In summary, the analyst should compile information on existing office supply using the categories listed above, both within the downtown study area and within the trade area. This should be done using an Excel spreadsheet to facilitate future data updates and analysis.

Additions to Supply

The projection of office space supply requires analyzing information on new projects, as well as renovations, conversions, and demolitions. Data on construction can be obtained through local assessors, and county or regional planning commissions.

Lease Terms

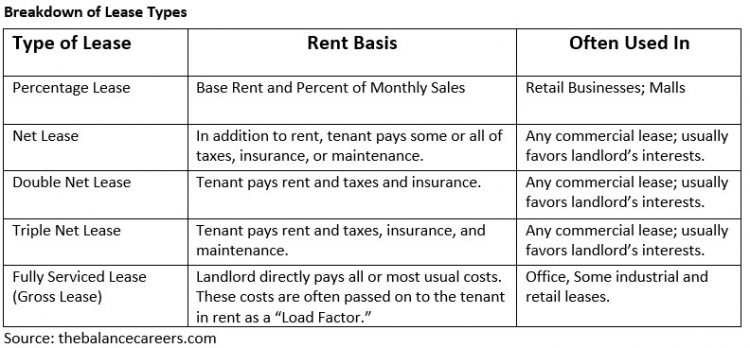

Lease terms are an important consideration for understanding of the existing and potential market for office space. They are important for developing an understanding of how downtown office space competes with other locations within a community and across the region or trade area.

Lease information can be obtained through public sources such as loopnet.com and from assessors, building owners, and leasing brokers. In compiling lease data, one should keep in mind that the data is often reported in different formats and presented in terms of monthly or annual rents per square foot.

Under a Triple Net Lease (NNN), the tenant is responsible for paying the building property taxes, insurance, maintenance, and repairs during the term of the lease. The rent charged in the triple net lease is typically lower than the rent charged in a standard lease agreement because the tenant is paying for the additional costs associated with managing the property.

Office Space Demand

Office space demand is a function of economic conditions including the local and regional business climate, population growth, and employment trends. These factors are essential in understanding historical and projected changes in business activity, office-dependent businesses, and community job creation. As previously mentioned, macro trends in office space demand have been changing since the Great Recession. Many companies have downsized in office space and do not see a need for more space with telecommuting and remote work increasing in popularity. However, demand has increased for collaborative and shared work environments and there continues to be demand for office space in downtown locations for some larger corporate employers as well as those predisposed to downtown locations such as accountants, lawyers, bankers, and dentists.

Location of office space and surrounding amenities are primary drivers of office space demand. Companies prefer office space located in areas with:

- close proximity to required business support services

- adequate and inexpensive parking

- convenient restaurants and retail outlets

- access to transportation networks such as transit, highways, major thoroughfares, and airports

Commercial real estate companies or similar organizations publish reports on national or regional office markets and while they are less relevant to small and medium sized downtowns, they are a resource to stay up to date on trends. Below is a link to a website that publishes quarterly reports on the current state of the national office market.

The COVID-19 pandemic has exasperated the situation of underutilized office buildings. During a period of remote work, the understanding of how/where we go to work has changed significantly. Many employees that have worked at home, find it very productive, and rewarding. This will likely continue to have an impact on the real estate market for office and workspace.

U.S. Market Reports

Tenant Type

It is important to be aware of the type and quality of tenants in a community because certain building types are better suited for different office tenants. It is essential to know what types of businesses currently occupy office space in order to project future demand for space. It is also important to consider who their clients are and why they chose their current location. According to Coldwell Banker Richard Ellis Group (CBRE), the following tenants lease the most office properties in the United States:

- high-tech

- business services

- financial services

- health care

- government

- insurance

- creative industries

- legal

Office space can also be divided into three types of uses:

- Activities that serve a non-local market such as regional offices of major corporations or financial services companies. This use is usually found in large cities but can also be found in smaller cities, one example might be the corporate headquarters of a locally based manufacturing firm.

- Activities that serve the local market such as accountants, bankers, dentists, doctors, insurance agents, lawyers, government, and real estate brokers. These types of office uses are common in small to medium sized downtowns, especially county seats.

- Light industrial businesses such as research and development companies or technology firms.

Analysis of Past Demand

Analysis of office space demand begins with an examination of historical office employment, occupied space, and lease rates. This information is used to make general inferences about office space demand. For example, if a community has experienced employment growth, low vacancy rates, and increasing rents over the last few years, it can be inferred that demand for office space is likely to continue increasing. Similarly, increasing vacancy rates and falling rents could be an indication of decreasing demand. This method of analysis infers future demand based on historical data and trends and cannot be completely relied upon. This method should be accompanied by professional interviews with local real estate brokers, developers, and business owners that have an intimate knowledge of the office market.

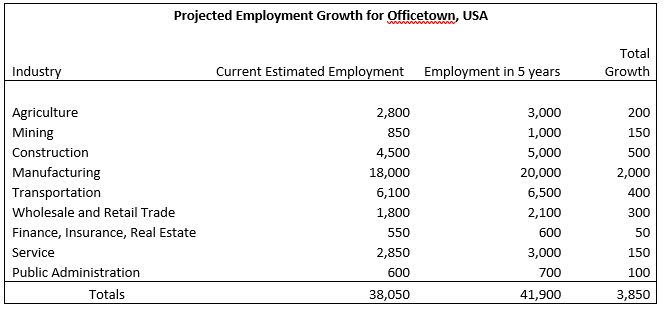

Sample Analysis of past office space demand for Officetown, USA

| 2009 | 2019 | Analysis | |

| Available Sq. Ft. | 6,000,000 | 6,5000,000 | Moderate increase in space |

| Vacant Sq. Ft. | 600,000 | 975,000 | Increase in vacant Sq. Ft. |

| Vacancy | 10% | 15% | Corresponding increase in Vacancy |

| Occupancy Sq. Ft. | 5,400,000 | 5,525,000 | Slight increase in occupied space (or 12,500 Sq. Ft. per year) |

| Absorption Sq. Ft. | 125,000 | Slight increase in occupied space (or 12,500 Sq. Ft. per year) | |

| Avg. Lease Rate/Sq. Ft. | $12.00 | $15.25 | Rates increased roughly 5% per year |

| Total Employment | 36,000 | 38,050 | Slight increase in employment |

Analysis of Future Office Space Demand

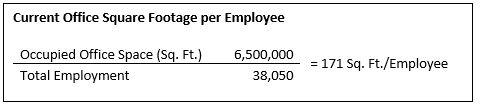

One of the primary influences of office space demand is the growth or decline of office-using jobs. Therefore, the ratio of occupied office space (in square feet) to total employment can be used to project future office space demand. This ratio multiplied by the projected employment growth for each year provides key insights into demand based on employment growth. If the data is available, this ratio should be calculated individually for each significant industry sector in a community. This will compensate for different office needs based on business type. Applying this ratio to industries driving office space demand will provide the best information to assess future office space needs. Demand driving industries will differ in communities, but they will commonly be finance, insurance, real estate, healthcare, and government. Also, this is a simplified analysis and may not be as applicable to small cities due data availability and limited employment in all industries.

One limitation with the ratio method is the assumption that the space needs of office employees and companies remain constant when in fact they may fluctuate. These methods also do not account for current office space trends. It has been widely published that square footage per employee is shrinking due to telecommuting, flexible work schedules, and shared work space. The shrinking square footage per worker trend will not have an immediate impact on smaller downtowns, but still should be kept in mind.

Changes in lease rates can also affect the demand for office space. For example, if vacancy rates are shrinking, this may cause an increase in market rent and potentially reduce office space demand.

Sample Projection of Future Office Space Demand

Step 1

Step 2

Step 3

In this example, it is estimated that Officetown, USA will need to accommodate approximately 658,650 Sq. Ft. of office space for the 10% employment growth over the next five years. This can be accomplished through absorption of vacant and new office space.

Public Institutions

Local, state, federal, and tribal units of government also generate demand for both new and rehabilitated office space downtown. A 2005 University of Wisconsin-Extension Report titled “The Importance of Government Facilities in Downtowns: An Analysis of Business Establishments in Wisconsin’s County Seats” found that,

“Public facilities are essential components of a healthy, strong and vibrant downtown. Many communities have seen economic and social benefits when the post office, municipal building, public library or other important public buildings stay or are expanded downtown.”

The report’s analysis affirms the merit of retaining major governmental activities in downtown areas. In many cases, these governmental functions are office-based and directly incentivize additional private sector investment in retail, restaurants, health care, and professional service establishments. Downtown analysts should therefore meet with local elected officials and staff to identify future downtown space demands for this sector of the office economy.

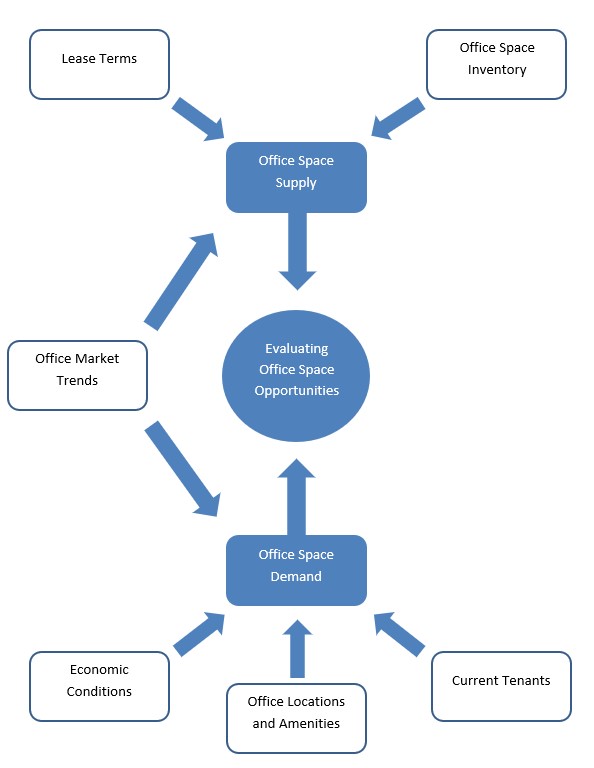

Evaluating Office Space Opportunities

Depending upon the results of the supply and demand analysis, the following methods for filling office space may be applicable to your community. It is worth repeating that downtowns in small to mid-size communities are unlikely to attract large corporations, unless these corporations are locally based. Typical drivers of office space are industries with local clients such as finance, insurance, real estate, healthcare, and government organizations. In addition, artists, entrepreneurs and startups may find downtown office space attractive under the right set of circumstances.

New Office Space

Given the current market, it would be risky for developers in most downtowns to build speculative office space. New private office space is now typically developed once a tenant for the space has been identified. In this case, downtown advocates should work with the community and developer to ensure that new office is developed in a manner that supports the overall objectives of the downtown district. For example, how can the new building be situated to maximize economic impact on surrounding downtown retailers and restaurants?

Rehabilitation and Retention of Existing Office Space

Converting underutilized space to office use through building rehabilitation is often more plausible for small communities than new office space construction. Small office space development could be an opportunity for some communities and usually involves the reuse of upper floors in existing downtown buildings. Although they would likely be Class B or C office spaces, office space in central business districts or other commercial areas could be a desirable and unique location for many firms. Many creative and professional firms seek these unique locations because of their central location and historical characteristics.

With building rehabilitation or repurposing, short and long-term attractiveness must be a consideration to assure tenant demand for the space. It is also important that office space be designed to match the typical office needs of prospective organizations. Trends affect average office space size and it is important to offer areas that are properly sized and have sufficient amenities to attract tenants. This also may affect the feasibility of which buildings can be repurposed to office spaces.

Shared Office Space

In addition to the traditional style workplace of multiple year leases, there are three other popular office styles that help support startup companies and entrepreneurs. They are business incubators, business accelerators, and co-working offices and all three can be successful methods to spur economic growth in downtown areas.

Business incubators are a way to provide office space or business expertise to startup companies through government, economic development, or academic sponsors. Typically, a sponsor partially or fully subsidizes the cost of office space and helps guide the company with business knowledge in market research, accounting, or other business services. Businesses would need to apply and be accepted into a business incubator program and would usually stay for a few years. In small town economies, small businesses that grow quickly have an immediate impact on the local economy through job creation and increased spending. Increasing business success rates through incubators may be an important tool for small communities.

Business accelerators, also called seed accelerators, are very similar to business incubators, but they differ in a few important ways. Business accelerators also provide office space and expertise to startups, but accelerator programs are very intensive and most business stay for a handful of months rather than years. Also, unlike business incubators, accelerators are hosted predominantly by private investors or businesses that are given company equity in return for their assistance.

Co-working space is a shared office normally used by small companies, independent workers, freelancers, and others who would usually work from home or be self-employed. Co-working facilities allow these workers to have an office away from home at the cost of monthly dues and it also creates a social and collaborative workspace for like-minded workers. It is also common for co-working facilities to have a value system and community building environments.

There are many successful incubators, accelerators, and co-working spaces throughout the country. A local example of a successful co-working space is called Rise & Grind and has a location in both Oshkosh and Green Bay, WI. They host approximately sixty members and pride themselves on offering weekly and monthly public events in addition to standard co-working uses of their facilities.

Rise & Grind: A Community Space

Developing Conclusions

Finally, it is important to develop goals and strategies based on office space supply, demand, and opportunities that make sense in your community. This is done at the broad downtown area level, and should not attempt to reflect individual projects which deserve their own feasibility study. While more detailed feasibility work may be needed, this assessment should provide business leaders with a preliminary market overview of office space development opportunities downtown.

Accordingly, general conclusions still become apparent through this level of analysis. Example conclusions could include:

- growth in demand for office space is likely to increase by X square feet in the next 10 years

- the growth and office space will accommodate X new employees to the downtown area in the next 10 years

- X new office buildings of approximately Y square feet each could be supported by the growth in demand

- older buildings and underutilized buildings representing approximately X square feet have the opportunity to be upgraded to class C or class B space, allowing it to attract additional new tenants and industries downtown

- the additional new and rehabilitated office buildings have the potential to draw significantly more employees downtown, representing a spectrum from entrepreneurs to seasoned and well-connected institutions.

About the Toolbox and this Section

The 2022 update of the toolbox marks over two decades of change in our small city downtowns. It is designed to be a resource to help communities work with their Extension educator, consultant, or on their own to collect data, evaluate opportunities, and develop strategies to become a stronger economic and social center. It is a teaching tool to help build local capacity to make more informed decisions.

This free online resource has been developed and updated by over 100 university educators and graduate students from the University of Wisconsin – Madison, Division of Extension, the University of Minnesota Extension, the Ohio State University Extension, and Michigan State University – Extension. Other downtown and community development professionals have also contributed to its content.

The toolbox is aligned with the principles of the National Main Street Center. The Wisconsin Main Street Program was a key partner in the development of the initial release of the toolbox. One of the purposes of the toolbox has been to expand the examination of downtowns by involving university educators and researchers from a broad variety of perspectives.

The current contributors to each section are identified by name and email at the beginning of each section. For more information or to discuss a particular topic, contact us.