March 2022 — Art and Entertainment events can draw people downtown and increase economic activity in a variety of business categories. These events can attract people downtown who normally would not visit. This section of the toolbox provides some initial ideas to help you begin to identify arts and entertainment development opportunities for your downtown. It includes identification of what makes up arts and entertainment and explains how you can use market analysis data to assess various activities and events.

Cultural Arts focuses on the community’s artistic talents that take the form of visual arts, theaters, dance, museums, or galleries.[1] Examples include: art shows/festivals/displays/galleries, author appearance/signing, ballet, book reading, chorus/choir, comedy, concert, dance, gallery night, museums, musical, opera, orchestral, symphony, and live theater among others.Arts and entertainment can be defined by a wide variety of activities. From dramatic ballet performances in a small downtown theater to colorful murals that dot downtown buildings, arts and entertainment can be brought to a community at almost any scale. For purposes of this section, we define activities of arts and entertainment as follows:

- Entertainment is an umbrella of a wide variety of activities, from a community plays to live bands, which energizes the downtown economy. Entertainment options can include: movie theaters (first and second run, independent, foreign and classic films), bands/concerts, karaoke, local bands, poetry/spoken word, stand-up comedy, parades, and street performers among others.

While arts and entertainment activities can add to a community’s sense of pride and quality of life, they can also contribute to local economic development. Cultural economic development can be defined as, “activities intended to promote increased market participation among traditional artists and arts organizations, as well as other arts and cultural organizations…”[2]

Market support for arts and entertainment events cannot be measured on a sales or square-foot basis. Accordingly this section provides ideas for examining the market using mostly qualitative data that have been collected in prior sections of the toolbox.

Demand for Arts and Entertainment

Data to describe market demand for arts and entertainment can include information on where your expected audience lives, who they are, and what types of activities they enjoy participating in. Different arts and entertainment activities can have different trade areas, so it is important to learn what types of venues people in your area find most appealing.

Arts and Entertainment Trade Area

The trade area for arts and entertainment activities may be different than your Trade Area(s) defined earlier in your market analysis. It is important to find where your potential attendees are from. This area is typically called a “destination” trade area, meaning that people may be willing to travel longer distances to attend art or entertainment events.

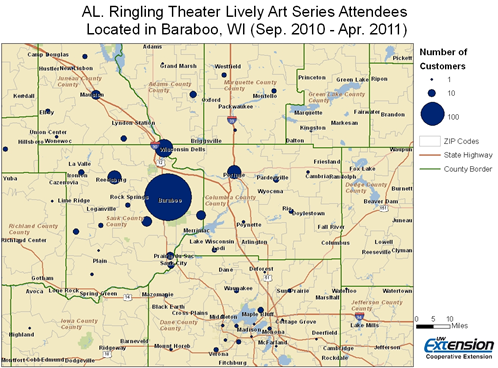

Below is an example of how the Al Ringling Theater in Baraboo, Wisconsin identified where their attendees were living. The zip codes were obtained from ticket sales and then mapped using Geographic Information Systems (GIS). This information was then be used to identify places that have high attendance that represent their arts and entertainment trade area.

Tourists and visitors also represent an important market segment for arts and entertainment activities. Often these nonresidents seek events that are authentic and that provide a memorable experience.

Demand for Movie Theaters From the ubiquitous movie palaces that dotted nearly every community’s downtown to the current rash of megaplexes with 16 or more screens on the edge of town, the movie exhibition industry has always had to adapt and change with the demographics, technology and demand from the community. A 2010 survey from the Motion Picture Association of America found that approximately 80 percent of U.S. movie theaters were located at sites that contained more than 5 movie screens.[1] While movie theaters can provide a viable entertainment option for keeping the downtown active in the evening, movie theaters are more than a social, cultural and entertainment outlet. They are also capital-intensive business with high operating costs. In some smaller communities, movie theaters do not survive as a business, yet are still operated as a service to the community often as a non-profit, a cooperative or a city-owned endeavor.

Demographics of Arts and Entertainment Participants

Demographics are an important factor in gauging what types of interests are associated with certain age groups and income levels. Some of the data needed for the arts and entertainment analysis may have already been complied in your demographic analysis (see earlier section of this toolbox).

As mentioned earlier, these activities could include events such as jazz, classical music, opera, Latin music, musical plays, non-musical plays, ballet and other dance. In order to understand what types of audiences attend these cultural activities, the National Endowment for the Arts (NEA) conducted a 2008 nationwide participant study. Listed below is part of the data that was collected by the NEA study and includes the highest participated art form, in a twelve month period, by many demographic categories.[3] These findings can help you determine the types of cultural arts that are preferred by trade area residents.

|

Activities in the Cultural Arts with Highest Participation |

|||

|---|---|---|---|

|

1st Choice |

2nd Choice |

3rd Choice |

|

| Age | |||

|

18-24 |

Musical Plays | Plays | Jazz |

|

25-34 |

Musical Plays | Plays | Jazz |

|

35-44 |

Musical Plays | Classical Music | Plays |

|

45-54 |

Musical Plays | Classical Music | Jazz |

|

55-64 |

Musical Plays | Plays | Classical Music |

|

66-74 and over |

Musical Plays | Classical Music | Plays |

| Education | |||

|

Some High School |

Latin Music | Musical Plays | Plays |

|

High School Graduate |

Musical Plays | Plays | Jazz |

|

College Graduate |

Musical Plays | Plays | Classical Music |

| Income | |||

|

Less than $10k |

Latin Music | Musical Plays | Jazz |

|

$10k to $20k |

Musical Plays | Classical Music | Plays |

|

$20k to $30k |

Musical Plays | Latin Music | Classical Music |

|

$30k to $40k |

Musical Plays | Jazz | Classical Music |

|

$40k to $50k |

Musical Plays | Jazz | Classical Music |

|

$50k to $75k |

Musical Plays | Classical Music | Plays |

|

$75k and over |

Musical Plays | Plays | Classical Music |

Musical plays, plays and classical music are the three most popular activities across all demographic categories in terms of cultural arts. Income, education, and age are strong indicators of what types of art and cultural activities will be attended by community members.

- Age – Generational differences will translate into different arts and entertainment attendance patterns. Participants who are currently middle-aged have the highest participation rates. It will be important to use your data from the market analysis to determine what age categories are in your community, and surrounding area, and how to gear your programming and marketing towards them accordingly.

- Education – Education is another factor you can use to help determine your community’s art and entertainment preferences. Similar to income, higher levels of education attained generally equates higher participation rates in art and cultural activities. Those who have completed some form of college and/or graduate level of schooling have significantly higher rates than those who have only completed high school or less.

- Income – Understanding local income levels is important in attracting people to arts and cultural events, and in determining what type of events they can afford. Income is a significant factor in terms of predicting arts or cultural participation rates. Across almost all of the art activities mentioned in this section, those making over $100,000 or more had much higher participation rates than those in the lower income brackets.

- Lifestyles – Marketing data firms such as Claritas and ESRI also produce a number of industry specific reports that describe arts and entertainment potential for a specific trade area. These reports provide estimates of market demand based on local demographic and buying power and combine indicators such as population, workplace population, income, wealth, home value, lifestyles, race, education and occupation.

As stated above, studies have shown that high income, high education and middle age can usually be equated with high arts and entertainment participation rates across most cultural activities. For example, in a participation survey done of 28 art and cultural organizations in Denver, Colorado, the average participant had the following characteristics.

|

Average Characteristics of Art and Cultural Patrons in Denver Colorado |

Average Characteristics of Residents in Denver Colorado |

|

|---|---|---|

| Median Age |

55 |

33.3 |

| Median Household Income |

$88,000 |

$45,438 |

| Education |

33% High School 38% College 24% Graduate |

23% High School 23% College 15.3% Graduate |

| Married |

72% |

40% |

Exhibit source: TRS Arts-Market Segmentation Study (May 2011)

The factors highlighted above by no means indicate that other demographic groups do not attend art or entertainment activities. They are simply the demographics groups with the highest participation numbers related to the cultural arts.

Demographics of Movie Theater Attendees

The Motion Picture Association of America (MPAA) publishes an annual movie attendance study entitled, “Theatrical Market Analysis.” While families, teenagers, college students and young couples are essential to movie ticket sales, it is important not to overlook any demographic. A community with a sizable retirement population may want to program special daytime screenings. The presence of a local film society could also encourage sizable ticket and concession sales at the movie theater. A large number of stay-at-home parents with younger children may support daytime programming of family films. A large teenage population may sustain midnight screenings on weekend nights. Collaborations with local groups and organizations along with targeted marketing and promotions may provide the needed boost in admissions. The 2011 MPAA Theatrical Market Analysis issued the following information about age demographics of those attending movie theaters in 2010.

- Ages 2 to 11 – 15%

- Ages 12 to 17 – 11%

- Ages 18 to 24 – 12%

- Ages 25 to 39 – 38%

- Ages 40 to 49 – 15%

- Ages 50 to 60 plus – 24%

Frequent moviegoers (those attending at least once per month in a year) make up 11 percent of total admissions. The most frequent moviegoers are those aged 25-39 years old (21 percent).

Using GIS to Estimate Where Theatre Goers May Reside

Lifestyle segmentation data and demographic data from firms like ESRI and Claritas can provide some insight on the geographic residence of potential theater goers. The key is to make sure that your assumptions regarding theater goers are accurate.

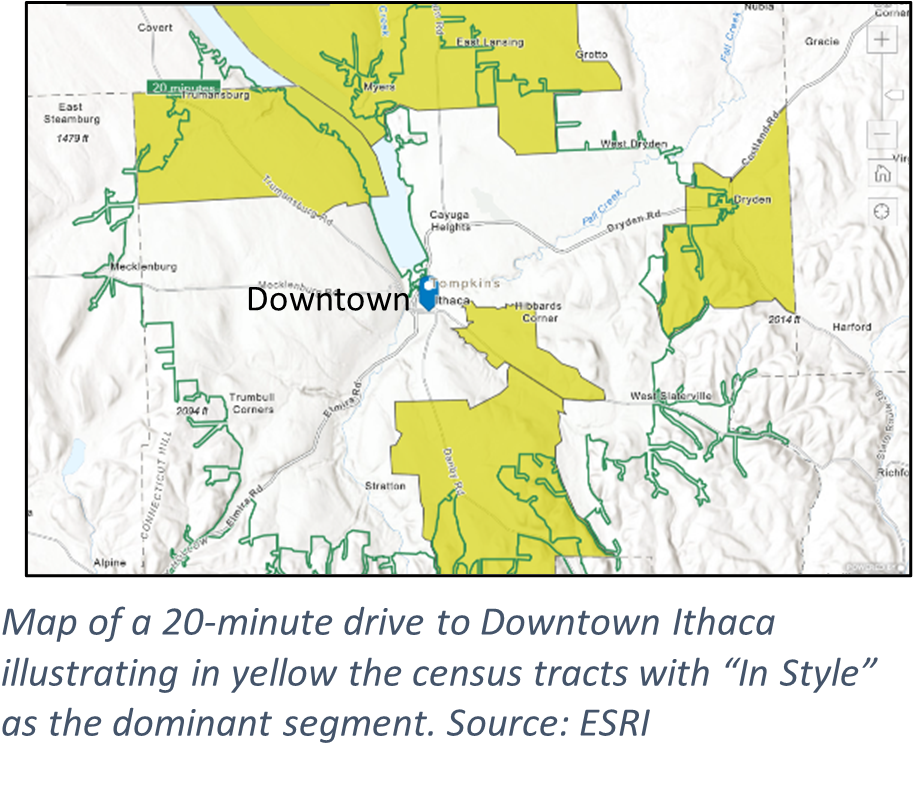

One category among ESRI’s lifestyle segments that participates in art and cultural activities is titled “In Style.” These households often support the arts, travel, and are extensive readers. Many have time to focus on their homes and their interests as they are slightly older and already planning for their

In exploring a 20-minute drive time area around a historic live performance theatre in Downtown Ithaca, New York, the accompanying map was created to highlight those census tracts where “In Style” is the dominant segment. Interestingly, the suburban areas around the community may have higher household attendance in the arts, but a lower number of attendees than the more urban and dense neighborhoods of the city. Theater goers in other lifestyle segments should also be included as potential participants in the arts, although maybe not to the same extent.

A complete analysis using lifestyle data should use the number of “In Style” households in all census tracts, not just where they are dominant. Furthermore, other lifestyle segments in the community may also have interests in theatre and should not be excluded.

The same kind of analysis can be done using demographic criteria such as age, income, education, and by type of activity such as attend the ballet or musical performance. The exact search criteria may vary from event to event, so lifestyle products can offer ongoing marketing research for diverse events as they are planned.

Surveys and Focus Groups

Surveys can help assess arts and entertainment demand specific for your particular community and/or trade area. These surveys should be conducted to study local and regional residents, daytime workers and night time visitor to your downtown. Questions could include:

- How often do you participate in these (list) arts and entertainment activities?

- Where do you typically go for these activities (list places)?

- How often do you currently come downtown for art or entertainment purposes?

- If you do not attend art or entertainment events downtown, please indicate why.

- What additional arts and entertainment activities would you like see available in the community?

Focus groups are another way to obtain information, viewpoints and attitudes about arts and entertainment activities in your community from local residents. If a downtown is without existing art or entertainment venues, focus groups provide an opportunity to drill deeper into some of the reasons why. Questions could include:

- Think about other downtowns where you may have seen a play or music performance. What characteristics of those places make them more desirable than our downtown? What characteristic of those places make them less desirable then our downtown?

- From your perspective, what do you feel are some potential barriers for attracting arts or entertainment venues to the downtown area?

Interviews with key members of the local arts community can also be used gauge local demand. These interviews can be conducted using the same questions listed above.

Available Arts and Entertainment Facilities

The evaluation of facilities available to accommodate arts and entertainment events is an essential next step. If appropriate spaces are not available (or cannot be developed), further analysis is not warranted. Each event type (live performance, comedy clubs, visual arts, etc.) will have its own set of location prerequisites.

Below is a list of some of the attributes that should be included in an inventory of downtown’s existing (or proposed) event facilities.

- Type of Space

- Name and Address

- # of Seats/utilization

- Outdoor or Indoor

- Ticket Prices/Covers

- Types of Entertainment

- Food or Drinks Served

- Other Rental Opportunities (describe)

- Other Unique Features (describe)

- Tie in with Other Downtown Businesses

- Complementary Businesses within the Downtown District (describe)

The information above is helpful in identifying potential space for new arts or entertainment events in your downtown. It is also helpful to examine how other communities have utilized their historic buildings and character to cultivate downtown art and entertainment activities.

Diverse Use of Theater SpaceThe Zona Gale Theatre in Portage, Wisconsin uses its space for a variety of art and entertainment venues throughout the year. The theater space is used for local concerts, youth productions, rental performances, summer theater performances and visual art gallery receptions. Other theaters such as the Mabel Tainter in Menomonie, Wisconsin rent their space for entertainment and non-entertainment uses such as weddings, business conferences and local fund-raising events.Space for other art and entertainment uses should also be examined. Gallery, studio, and practice space may be needed, often at subsidized rental rates. Side-streets and second floor space is often suitable and proves adaptive reuse opportunities for downtown.

Assessment of Arts and Entertainment Opportunities

The final part of this assessment involves reconciling the market data collected and developing conclusions regarding new arts and entertainment activities and events. Identification of ideas that are authentic to the community can help create an entertainment destination. However, one should be cautious not to have a “if we build it, they will come” mentality when developing ideas.

To determine what carts and entertainment ideas have the greatest potential, answer the following questions:

- What is the geographic origin of potential customers? Does this change by season?

- What do local demographics and lifestyle characteristics suggest about market demand for art and entertainment experiences from local residents? Visitors?

- What other related businesses (such as restaurants) are missing from the downtown district that would otherwise complement arts and entertainment events?

- What are the best practices from other similar communities?

- What are the assets (history, character, sense of place) that can be used to promote downtown a cultural or entertainment destination?

- What do our assets suggest about potential opportunities for new art and entertainment events?

- What mix of events would be necessary to create a critical mass of arts and entertainment activity?

Without having a comprehensive assessment of your downtown’s art and entertainment needs and opportunities, decision makers may gravitate to catalytic, large-scaled and expensive projects for their downtowns which may not be feasible. Decision makers may want to build upon the art and entertainment offerings already available in their community.[4] Opportunities for downtown arts and entertainment may include the desire to expand a community theater or art program, the ability to capture the cultural heritage of a community or to incorporate new art or entertainment forms into the downtown.

Because of the complexity of the arts and entertainment, this analysis is not intended to be a complete market feasibility analysis. Instead, its purpose is to help the user begin to identify possible arts and entertainment development opportunities. Ideas identified in the analysis will require a more detailed study.

[1] Schuster, M. 2000. The Geography of Participation in the Arts and Culture. National Endowment of the Arts, Research Division Report #41. Santa Ana, California: Seven Locks Press.

[2] Chris Walker, Maria Jackson, Carole Rosenstein, “Culture and Commerce: Traditional Arts in Economic Development” The Urban Institute and The Fund for Folk Culture (2003) 12.

[3] 2008 Survey of Public Participation in the Arts. National Endowment for the Arts, Research Report #49.

[4] Marksuen, Ann, and Anne Gadwa. “Arts and Culture in Urban/Regional Planning: A Review and Research Agenda.” Project on Regional and Industrial Economics in the Humphrey Institute of Public Affairs. Working Paper # 271 (2009)

About the Toolbox and this Section

The 2022 update of the toolbox marks over two decades of change in our small city downtowns. It is designed to be a resource to help communities work with their Extension educator, consultant, or on their own to collect data, evaluate opportunities, and develop strategies to become a stronger economic and social center. It is a teaching tool to help build local capacity to make more informed decisions.

This free online resource has been developed and updated by over 100 university educators and graduate students from the University of Wisconsin – Madison, Division of Extension, the University of Minnesota Extension, the Ohio State University Extension, and Michigan State University – Extension. Other downtown and community development professionals have also contributed to its content.

The toolbox is aligned with the principles of the National Main Street Center. The Wisconsin Main Street Program was a key partner in the development of the initial release of the toolbox. One of the purposes of the toolbox has been to expand the examination of downtowns by involving university educators and researchers from a broad variety of perspectives.

The current contributors to each section are identified by name and email at the beginning of each section. For more information or to discuss a particular topic, contact us.