(Image Source: RunnyRem / Unsplash)

How COVID-19 has impacted the Wisconsin lodging Industry

May 2022 — Hotels provide an important service to our communities and represent a significant economic engine for jobs, business revenue, and taxes. Plus, they often serve as a gateway to a community, influencing perceptions of the broader community.

However, this industry has experienced significant challenges due to the pandemic and changing travel behaviors, both in the US and in Wisconsin. While historically a volatile real estate asset, hotels can provide a favorable return on investment, based in part on room rates, occupancy levels and cost controls.

In this issue of Downtown Economics, we start with a summary of US trends in lodging based on the recently released Outlook 2022 published by the American Hotel and Lodging Association. Specifically, we summarize the work provided by this organization in measuring year-over-year activity and changes in the market. Based on the AHLA trends, we examine Wisconsin trends as shared by two hotel experts who have each devoted 30 years of their careers to the development of hotels in Wisconsin and beyond. We close with a few ways the industry may change as a result of COVID-19 and other global issues.

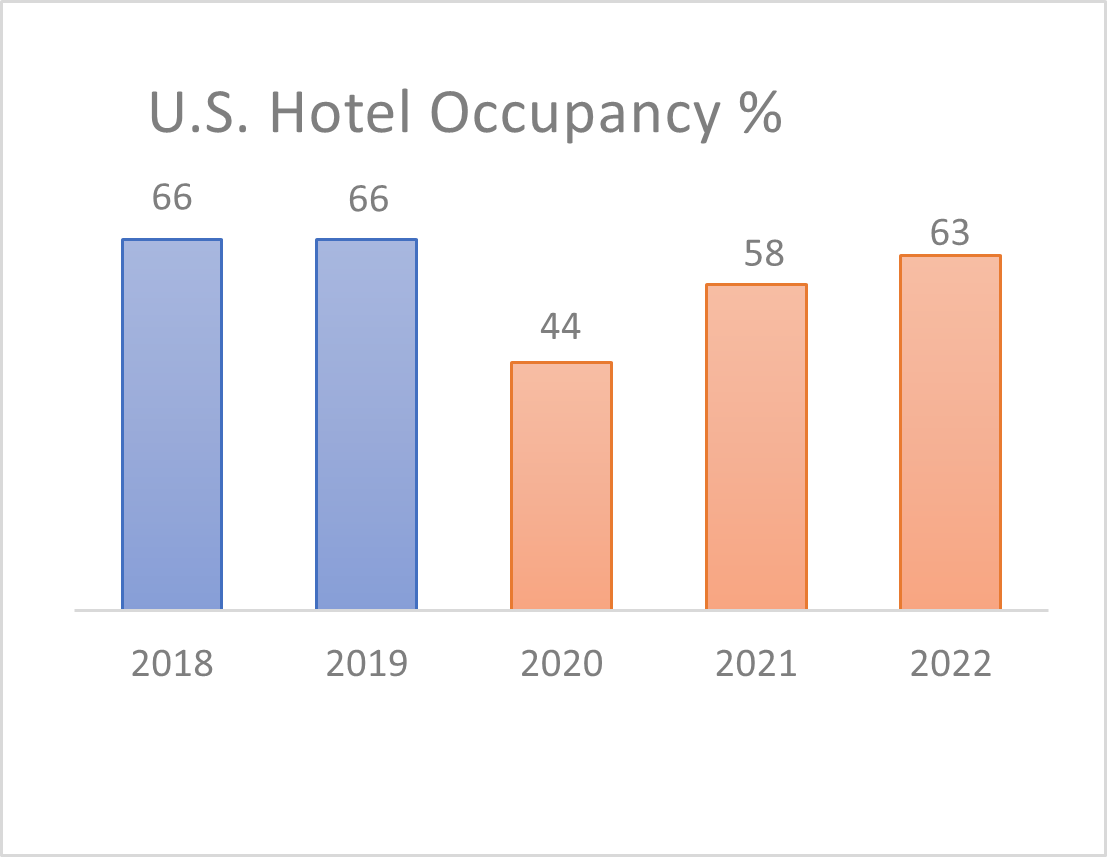

U.S. Hotel Industry Report

The U.S. hotel industry is expected to continue moving toward recovery in 2022, but many uncertainties lie ahead. Full recovery is still several years away.

The American Hotel & Lodging Association has recently published its 2022 State of the Hotel Industry Report. It reveals how consumers have changed their overnight travel from before the COVID-19 pandemic in 2018 and 2019, through current year estimates for 2022. The accompanying bar chart shows a significant drop in U.S hotel occupancy in 2020. These estimates were assembled in collaboration with AHLA Silver Partner Accenture and is based on data and forecasts from Oxford Economics and AHLA Platinum Partner STR.

U.S. Hotel Occupancy, 2018-2022

The top findings of the report as reported by AHLA include:

- US Hotel occupancy rates and room revenue are projected to approach 2019 levels in 2022.

- The outlook for ancillary revenue, which includes food & beverage and meeting space, is less optimistic

- Hotels lost a collective $111.8 billion in room revenue alone during 2020 and 2021

- Leisure travelers will continue to drive recovery: in 2019, business travelers made up 52.5% of industry room revenue; in 2022, it is projected to represent just 43.6%

- Business travel is expected to remain down more than 20% for much of the year, while just 58% of meetings and events are expected to return; the full effects of COVID-19.

- Changing traveler segments, including the rapid rise of B-Leisure travelers—those who blend business and leisure travel—are impacting how hotels operate.

Wisconsin Trends

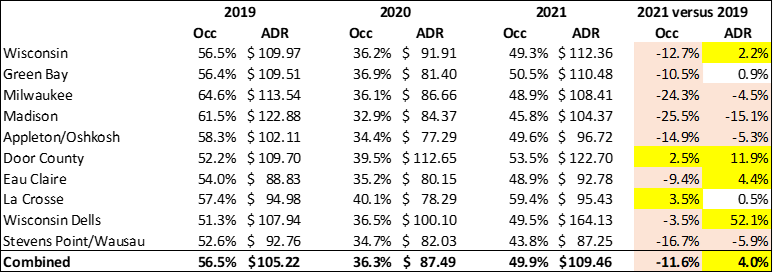

Data collected and analyzed by Michael Lindner of Wisconsin-based Hotel R&D, LLC presents lodging performance in Wisconsin and key travel destinations from 2019 to 2021. The table indicates that hotels, motels and resorts in most market areas and Wisconsin as a whole, exceeded 2019 average daily room rates (ADR). Occupancy levels (Occ), in contrast, continue to lag 2019 largely due to the slow recovery of business, individual and group travel. This is similar to the US performance trends.

The growth of ADR in 2022 is expected to continue but at a considerably slower scale. Hotels in vacation destinations such as Door County and Wisconsin Dells pushed the rate considerably higher due to the combination of strong demand and higher operating expenses. At the same time, hotels in business destination markets continue to discount their rates to attract a greater share of leisure visitors to compensate for the slow recovery of business travel. Yet business travel is recovering and should result in an uptick in ADR in the larger urban centers.

1. Variation in occupancy and rate among Wisconsin cities

Occupancy growth in the select communities presented in the table below is expected to become more balanced between the vacation destinations and the corporate demand-based cities. Significant increases in gas prices and general economic instability could even result in lower occupancy levels in places like Door County and Wisconsin Dells.

Still, Wisconsin Dells and its leisure travelers experienced a significant increase in room rates. In two years from 2019 to 2021, the average room rate in Wisconsin Dells increased from $108-$164, or 52%.

However, some corporate destinations are experiencing a growing “back-to-the-office” trend, at least by major employers. The theory for hotels is that as employees return, so will out-of-town visitors.

Wisconsin Lodging Industry Trends in Occupancy and Average Daily Room Rate

Note: The significant increase in Wisconsin Dells ADR may be the strength of the higher-end waterpark resorts performance over the other franchise and independent properties in the area.

2. Wisconsin operating performance based on room tax collections

Hotel room tax collections in Wisconsin were analyzed by Michael Lindner of Wisconsin-based Hotel R&D, LLC. A review of hotel room tax collections from 2016 – 2021 (based on those communities reporting) also includes marketplace rentals (Airbnb, VRBO, HomeToGo, etc.). Key findings include:

- Lodging revenues of hotels, motels, inns, marketplace rentals) that reported data decreased by 38% in 2020 from 2019.

- Of the 166 reporting communities for 2021 (54%), revenues increased by 75% over 2020.

- If lodging businesses in the remaining communities experienced similar increases as the reporting districts, lodging revenues for 2021 will exceed 2019 revenues by over 18%.

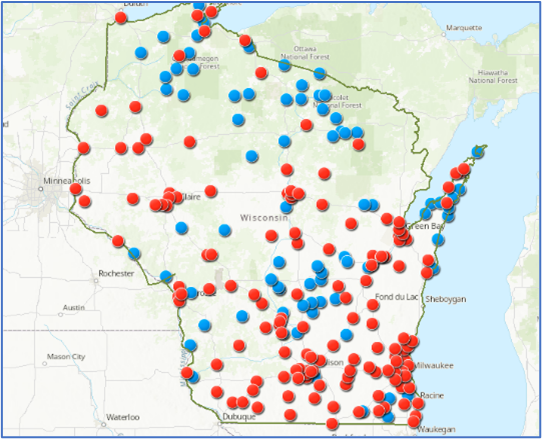

Despite the significant losses in room tax collections in 2020, there were communities that reported increases. The map below illustrates in blue those communities with higher room tax collections in 2020 over 2019. The red communities had lower tax collections in 2020.

While the location of room tax growth appears to be spread throughout the state, the regional separation offers a more telling story. Communities that reported increases in room tax collections in 2020 over 2019 had an average population of approximately 3,000. The heaviest concentration of communities was in far northern Wisconsin. The next largest cluster of communities is in central Wisconsin including Adams and Marquette counties (but not Wisconsin Dells/Lake Delton). Door County and the Driftless Region of southwest Wisconsin were similar in the number of communities with room tax growth.

Wisconsin Room Tax Collection, 2019 & 2020

This activity coincides with the surge of demand for smaller rural surroundings with outdoor recreational and relaxing environments. The surge was likely triggered by the “stay home” mandates during peak COVID-19 months. Demand was generated by a remote workforce as well as furloughed employees and those merely seeking an escape from the year’s issues.

3. The growing popularity of marketplace rental units in Wisconsin

The positive room tax collections were also a result of more communities seeking tax compensation from marketplace rental units. The popularity of single-family dwellings, including private homes, cottages and cabins soared in 2020 and will continue to have an effect on the more traditional hotel industry.

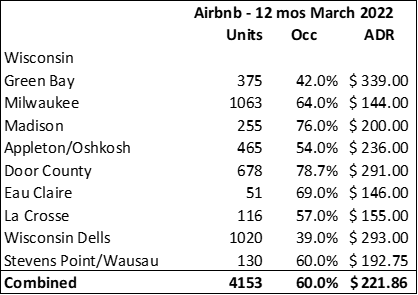

Somewhat related to marketplace rentals are extended stay hotels with home-like amenities. These products, under various brands, have outperformed other product categories over the pandemic. The following table offers a review of Airbnb and related rentals’ performance in the same markets previously listed at the beginning of this section. The performance statistics are for the running 12-months through March 2022.

Marketplace Rental Performance

Compared to the hotel performance table presented earlier, marketplace rentals achieved an occupancy level of 60% (compared to the 2021 hotel performance of just under 50%). Average rates were $221.86 for marketplace rentals in 2021/2022 compared to $109.46 for hotels in 2021. The popularity of Airbnb and other similar rental programs can be a concern for the more traditional lodging operators. It can also open the doors of opportunity for those traditional hotels to rethink standard operating procedures and design templates.

4. Changes in market segmentation

Behind hotel performance is a significant change in market segmentation among hotel guests. COVID-19 has impacted market demand, reducing business and group travelers, while increasing tourist and leisure travel. One new hybrid market segment is called “B-leisure travelers, those who combine both leisure and business travel. As a national trend, it is also occurring in Wisconsin.

During the pandemic, urban hotel markets saw occupancies drop to unparalleled levels as stay-at-home mandates forced many hotels to close from March to June 2020. Even as they reopened, business and leisure visitors opted to avoid more densely populated centers and large city hotels. Instead, business travelers able to participate in the new practice of “remote” working, flocked to less populated areas that offered isolation yet enough conveniences to perform necessary business functions.

While the pandemic is often credited with the rise in B-leisure travel, the phenomenon also referred to as “biz-cations”, has been a subtle demand market for many years. Historically, mixing business and leisure travel was associated with larger established destination markets known for entertainment, recreation, and sightseeing. Today, and a direct cause of the Covid-19 economic shift, many of the sought-after destinations are more secluded and offer tranquility and spiritual renewal as well as recreational experiences.

This same focus on individual B-leisure travel has helped to facilitate the return of the corporate group segment of hotel demand. A survey conducted by STR/CoStar Realty performed in 2021 asked 900 meeting planners a series of questions regarding their plans for post-pandemic group meetings. Responses indicated that future group functions will create:

- Smaller regional meetings held within driving distance of their businesses or residence

- Meetings at smaller hotels in smaller markets

- More outdoor meetings and meetings in non-hotel venues

Still, the ability to house these groups within the same general location will be vital to the success of this trend. Lodging operations that can cater to groups, provide technological amenities, and offer a range of recreational and “spiritually uplifting” experiences will find a growing audience of both business and leisure visitors.

5. Future hotel development in Wisconsin

Richard Sprecher reports that the pipeline of activity has slowed, but developers are still preparing for reentry with new, innovative proposals that will help make lodging a more integral part of the community.

Lodging growth in the supply of new rooms was at a peak from 2017 – 2019. However, industry growth (like industry performance) is often measured by activities in the country’s top 50 markets. Large urban metropolitan areas set the standard for strengths or weaknesses in hotel development as well as the measure of occupancy and average daily rate.

However, at the same time, an emerging trend toward hotel development in secondary and tertiary communities was in progress. As communities re-established their focus on downtown districts, overnight accommodations have become an important component in the placemaking of downtown. In some small towns, leisure and business visitors also sought the experience of a hometown atmosphere where they can walk to unique and independent shops, services, restaurants, and other amenities.

With the possibility of continuing inflation and higher interest rates, coupled with higher construction costs, the growth of the supply of lodging products is still uncertain. The increased use of green technology will help contain construction and operating costs while contributing to environmentally responsible development.

Looking Ahead

Wisconsin will likely follow many of the national trends in the hotel business. In the AL&HA report, Liselotte De Maar, managing director in Accenture’s travel industry report believes that cleanliness and sustainability have become important in traveler decision-making. Today’s traveler expects a cleaner experience. Related to that are more ways to connect digitally with your hotel services and amenities.

Lodging product popularity is also changing. According to Richard Sprecher, the current trend in Wisconsin and other midwestern states is smaller hotels that have a need for a smaller workforce. In the limited-service lodging business, the largest operating expense is labor. Extended stay-type hotels have become the most active segment in hotel development due to their small staff, ease of operation, and appeal of home amenities such as a full kitchen.

Many are also using “smart hotel” technology for check-in, messaging, remote key lock, and access to staff. With the diversity of the hospitality industry, the personalization of services is now an expectation at some properties.

The consulting firm Deloitte US describes future hotels as being more about people, centered around customer experiences and connecting with people. Even as new technology, evolving customer preferences, and new competitive threats change the hotel experience, outstanding hospitality will still require a thoughtful human touch. The hotel of the future will offer guests a memorable hotel experience tailored to their unique preferences.

Takeaways

Hotels are an essential amenity to attract tourists and visitors to your community. They can be risky investments, especially in times of economic uncertainty as demonstrated by the COVID-19 crisis. Consider the following takeaways as your community considers new lodging accommodations for its visitors and for overall economic development.

- The US hotel industry was significantly impacted in the year 2022 by COVID-19. However, hotel room occupancies are increasing, and are now approaching pre-pandemic levels. While business travel and convention travel volume have decreased since the pandemic, leisure travel and a combination of leisure and business (B-leisure) have gained traction and have helped increase both room rates and occupancy, especially in rural areas and resort communities.

- Wisconsin hotel performance is also recovering. While occupancy levels have increased since 2020, the average room rate has increased more, especially in resort and rural destinations. If average room rate increases do not decrease occupancy, then the incremental benefit of raising prices falls right to the bottom line as there are no attached variable costs associated with each additional dollar charged.

- Wisconsin lodging performance, beyond hotels, includes an increasingly popular type of overnight accommodation called a marketplace rental (such as Airbnb). These lodging units are gaining popularity by serving a growing leisure segment of travelers.

- The development pipeline for new hotels remains cautious, though the development community is actively looking for opportunities that will accommodate changing traveler preference. These opportunities might include properties that serve the B-leisure market, and provide homelike amenities, possibly in vibrant downtown locations in smaller cities.